The hard thing about investing in hardtech

This is a continuation of the previous post. In the previous post, we covered what kind of technologies constitute hardtech, what is different about developing and commercialising such technologies. Read the first article here.

Venture capital for technology has evolved over its lifetime. Over the last three decades, most venture capital has moved away from being at peace with significant technical risk to seeking early-stage startups with hitherto unmitigated market risk or slightly more mature startups needing capital to scale quickly.

Yet, history is replete with venture capital being deployed to develop technology often from scratch or without much precedent.

Fairchild Semiconductor, one of the first venture-backed semiconductor startups in California, performed their entire product development on venture capital. The prevailing science of the era was to fabricate transistors out of germanium. Though silicon was better than germanium on every relevant metric, silicon production workflows hadn't matured.

In part this was due to the lack of attention silicon had received until that point. Most semiconductor companies of the era were building towards a germanium future. The 8 founders of Fairchild Semiconductor made the decision to base their product on silicon. In the early days, it seemed like a choice doomed to fail. After all, a silicon transistor cost $ 14.53 and a germanium one could be bought for $ 1.93!

In 1957, on a $1.5M seed investment facilitated by Arthur Rock and funded by Sherman Fairchild (of Fairchild Camera, New York), the Fairchild Semiconductor team started working on their silicon transistors. In two years, they had carved a path to market. By 1959, the company was making $3M in revenue at 10% margin. As technology progressed, by 1965, the price of a germanium transistor had dropped to $ 0.50. Fairchild was selling silicon transistors for $0.75. During the same period, the unit sales of germanium transistors had risen from 119 million to 334 million. In contrast, the unit sales of silicon transistors during the same time had leaped from 9 million to 273 million. In the next 10 years, silicon transistors dropped below $ 0.01 and germanium was sidelined forever.

Today, outside of core biotech, this kind of R&D activity is seldom done with venture capital. Yet, the roots of venture capital lies in such technological derisking being expedited through private investment. In fact, let’s dive right into a biotech story.

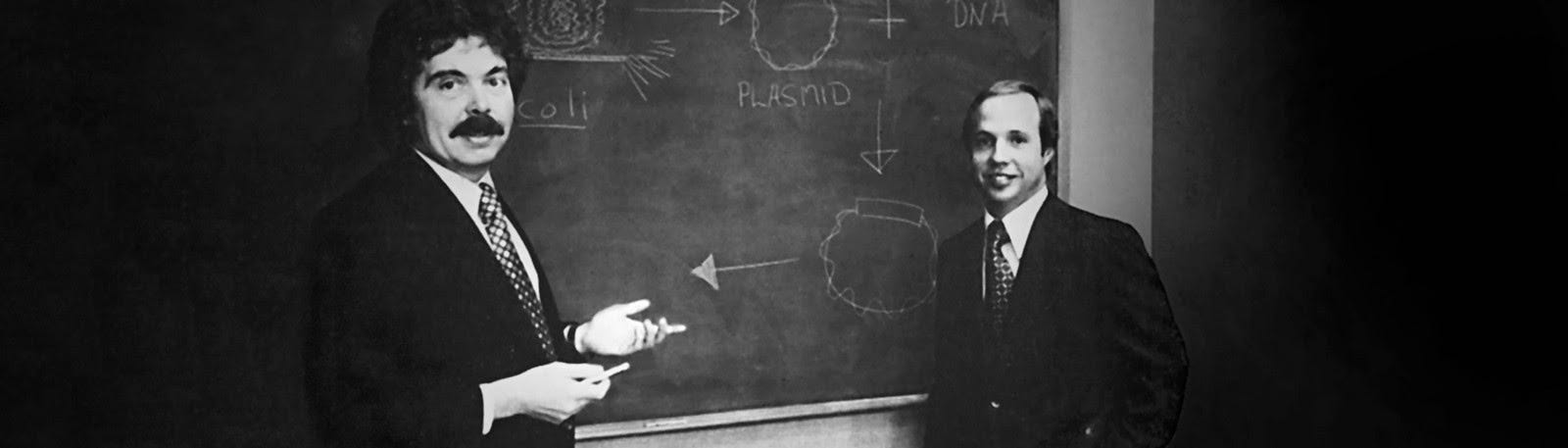

Genentech, founded in 1976 as the pioneer of biotechnology in the US, used venture capital for academia-level research. No one had shown that it was possible to manufacture a human protein in E Coli. To gain credibility as a biotechnology company Genentech decided to demonstrate the production of human somatostatin in E coli bacteria. They called it an “academic exercise” with no practical merit, but it was an important and necessary first step - to show investors that the technology could work. The National Institutes of Health (NIH) had just rejected a proposal to do just that experiment. Why would the investors believe this team over the NIH’s scepticism over the entire concept in general? This made this particular proof-of-concept demonstration all the more critical. Succeeding in this demonstration brought Genentech no revenue whatsoever. But it established beyond doubt that this team was going to be a trailblazer.

The team decided to focus their attention on diabetes. Until then, the only way to manage diabetes was to produce the insulin patients needed in cattle and pigs. The problem was that this insulin wasn’t really human per se. People needed multiple injections per day, faced a risk of adverse reactions and to top it all off, production was highly expensive. Being able to manufacture human insulin in E coli was seen as a disruptive innovation. It would immediately solve the effectiveness and cost problems. The only problem: no one had done anything of the sort. In 1978, Genentech announced that it had succeeded in producing human insulin in E coli. It is estimated that almost $ 100M was required to develop this first product for which Genentech would finally gain regulatory approval in 1982. Most of this capital was provided by VC firms.

Despite these successes, why did venture capital move away from technical risk?

Broadly, I see three reasons for this shift:

Path to market is much shorter and easier with non-hardtech offerings:

Investors love to guess. But they love proof of traction even more. It is much easier to get a sense of the market’s reaction to the product if you can put a beta version into the hands of the user. For a hardtech offering, it will typically require ~ 5 years before any sort of meaningful data from the market interaction is available. Let’s put this in perspective. Evan Spiegel launched the first version of Snapchat within 3 months of conceiving of it. Within a year, Snapchat was processing 20 million images per day. Berkeley Lights was founded in the same year, 2011. They were building a platform that would shrink development timelines of therapeutic antibodies and cellular therapies by orders of magnitude. Their first product was rolled out in 2016, five years from company formation.

Large businesses have been and can be built in non-hardtech areas:

The internet boom in 1990s and the smartphone boom in 2010s were inflection points that resulted in massive expansions of the available market. When billions of people came online and then subsequently went mobile, a tremendous amount of market potential was unlocked. Expectedly, founders built venture-backed businesses targeting different facets of the customer needs. Many of these companies had successful outcomes. Consequently, more founders rushed in and to support them, more capital. A virtuous cycle was set up. Not surprisingly, over the last two decades, VC firms have been flooded with investment opportunities wherein the tech risk is minimal.

It can be difficult to perform due diligence on hardtech startups:

The typical VC firm is not equipped to do the same sort of diligence for hardtech as they can perform for other kinds of businesses. Compared to the internet boom, the ecommerce boom and the smartphone boom, there has been no hardtech boom per se. There have only been scattered instances of successes, almost like punctuation to a string of successes for other kinds of businesses. By contrast, the same virtuous cycle that has led to sustained hits in the internet and software sector has created a deluge of experts in the form of exited founders, successful investors and even failed founders. VC teams are stacked with such experience. They can understand, evaluate and even troubleshoot these types of startups from the wealth of their shared experience. Additionally, the culture of openness in the form of content marketing by leading VC firms have further democratised access to such assessment metrics. Nothing like this has happened for hardtech startups. As a result, running due diligence for hardtech has remained difficult, shrouded in secrecy and quite confusing.

Hardtech can also be quite specific. Understanding the technical risks and then the subsequent moat would require significant technical depth. In-house diligence processes may not suffice. If you are a SaaS investor, you can, practically, grasp any SaaS business with some effort. All the different SaaS startups you see are more alike than they are different. On the other hand, most hardtech startups will be very different from each other in terms of their objectives, approaches, technologies, moats and of course, GTMs.

As a result, most investors struggle with the question: do I get it?

Ultimately, the decision to invest in hardtech boils down to understanding the risk profile associated with every individual venture. In absence of enough data (compared to other ventures), the fear of losing can dominate the desire to take big risks for bigger rewards. LPs invest in VC funds not only for the growth opportunity but also to protect their capital from short-term market volatility. It is true that hardtech startups are more resilient. Since the product offering is usually serving a critical need (for example, cheap energy) or a long-desired aspirational technology (for example, electric vehicles), they are more immune to unexpected events like political change or pandemics. Yet, they also require large amounts of capital to get off the ground, sustain and finally succeed.

And herein, lies the source of the quandary: how do we balance the risks of something we can’t fully appreciate?

Risks

The commonly thrown around adage about hardware in general is that “hardware is hard”. It is easy to imagine the rhetoric around hardtech (which carries even more technical risk than general hardware) with this background. While I will accept the general sentiment that finding success in this domain is difficult, I will push back on the claims that the rates of failure are any different from non-hardtech. I am yet to see any comparison that proves otherwise. In a sense, it might be that hardtech startups trade some amount of market risk for taking on higher technical risk and on the whole, over a long enough time horizon, this evens out. A point to note is that the hardtech wave is just about getting started and it might take a while for meaningful data to be compiled and made available.

For an investor, the risks of a failed investment come from several aspects:

Insufficient derisking of the technology: there are multiple ways that a technology can fail in its journey from conception to productization. Not all of them are obvious at conception or even the early prototyping stages. Additionally, the end of lab-scale technology development is not an end in itself. The startup will then have to establish and derisk the entirely novel supply chain to move at scale. Simultaneously, the founders will also have to figure out their regulatory pathway to approval if they are in a monitored space.

Inability to recruit proper talent: when building a product with high technical risk, there is simply no better asset to acquire than talent. Yet, early stage founders can have limited reach in order to find the talent they need and properly vet them. Without proper talent, the chances of success can dwindle significantly.

Inability to raise strategically aligned, patient capital: the proliferation of the VC ecosystem around the software, internet and smartphone booms have optimised the fund structures to work extremely well for generalist tech startups. With 10 year life cycles, VC firms struggle to find patience amidst the market frenzy. Hardtech moves slowly because a whole lot of building is involved before the next milestone. “Move fast and break things” is terrible advice for hardtech. As an investor, you would need to recognise the limitations of the world of atoms as opposed to the world of bits. This can be more challenging as the company grows and needs more such investors who recognise the specific risks and limitations. Expectations misalignment can create existential threats to the hardtech startup.

Rewards

VCs know that success of a hardtech startup comes with tremendous returns. Quantumscape, building the world’s most efficient batteries for the EV revolution was founded in 2010, raised a total of $ 300M and went public in November 2020 through a SPAC, being valued at $ 3.3B (currently, $ 11B). BioNTech is the company behind the leading COVID vaccine candidate. It was founded in 2008 and raised about $ 650M before going public in Oct 2019. It is currently valued at $ 25B.

Beyond the immediate fiscal gains, the portfolio construction gets a complete makeover. Bear in mind, an overwhelming majority of VC firms are not used to investing in hardtech. The timelines associated with a hardtech startup’s path to market, the patience it would require to systematically derisk different aspects of the offering and the (perceived) amount of cash infusion the startup would need before a product can be monetised are enough reasons to spook most traditional investors, who would prefer a venture with lower technical risk.

On the other hand, it is no secret that investing in non-hardtech (essentially, everything else) has become fiercely more competitive over the last two decades. With companies staying private longer, private equity firms have been gradually eating into late-stage VC. As a result, late-stage VC firms have started migrating towards earlier stages. With this kind of downward pressure, the whole investment stack gets pushed to earlier stages. The result: in 2010, there were 33 seed funds; in 2020, there are more than 800. (US-only data)

Being known as a patient investor who understands the specific demands and challenges of being a hardtech supporter is a crucial differentiator. When done right, hardtech successes are fertile ground for the germination of new startups. Ambitious people with unparalleled experience in development of pioneering technologies will branch out with their own endeavours. If an investor of their previous employer has been praised for their support of a hardtech startup, this reputation can be an oasis of hardtech dealflow.

Moreover, success in hardtech is built on the foundation of proprietary technology protected by massive IP portfolios which translate into high entry barriers for upcoming competition. Coupled with well-thought out business models (sometimes radically novel) and a huge unmet market need, these conditions are perfect for establishing large, enduring, monopolistic companies.

Illumina raised about $ 30M before going public in 2000. The stock dropped from $ 20 to $ 1 due to the dot com bust, soon after. Yet, 20 years later, the stock is valued at about $ 300 and Illumina remains the unequivocal market leader in DNA sequencing. We can also look at Tesla. Since the IPO in 2010, the stock has multiplied over 150X. 15 years after they made the first EV, they are still, by far, the market leader.

Give me feedback about the length of each post. Take a one question survey.

In the next part, I will write about how building hardtech is starting to become somewhat easier to build.

If you have any feedback, I would love to hear from you.